Most Valuable Capital

In the 21st century, what is the most valuable capital we have, beyond our prized human relationships? We are conditioned to believe that the most valuable capital is financial in nature or manifest as physical assets with monetary value. Witness the somewhat irrational rush for gold assets in recent years or a frenzied craze for owning multiple residential and commercial properties across the world! The truth is that as we have been evolving rapidly as a global civilisation, the most valuable capital we possess right now is increasingly non physical. Digital Capital's value per gram can be infinite because it is weightless! The more creative the Digital Capital, the more infinitely valuable it becomes!

How to Secure Digital Capital?Innovation, Dynamism and Flow

This Digital Capital adds value when it is innovative, dynamic and flowing. When we buy most new products, services and solutions -- tangible or intangible -- what we are paying for in terms of utility, design and functionality, is primarily a manifestation of Digital Capital -- a type of concentrated human intellectual creativity -- and not financial capital. Although, finance may have had some part to play in its creation as catalyst. Such is the power, reach and richness of Digital Capital, that most of the time old-fashioned finance and money also manifest as Digital Capital. All our bank accounts, no longer have physical ledgers beneath them, they simply exist by virtue of a digital data entry against our name. The same with most bonds, shares and other financial instruments.

Human-Like Personality

The chief characteristic of Digital Capital is that it is useful, and adds value, if it is capable of being in motion. If any Digital Capital goes into hibernation, remains dormant, stagnant or cannot be accessed, it diminishes in value and tends towards zero value very fast. Live Digital Capital is much more prized than dormant, corrupted or dead Digital Capital, just like human beings. If Digital Capital falls into the wrong hands, it can appear as if humans have been kidnapped and are being held to ransom! Digital Capital is not the same as money, gold or other physical assets falling into the wrong hands, which are all replaceable. Digital Capital carries unique attributes and qualities that render human-like personality to it and this makes Digital Capital fundamentally irreplaceable.

Instant Remote Access

If we look back a few years -- any time one wanted to type a letter, create a spreadsheet, edit a photo, or play a game, one had to go to the computer vendor, buy the software, and install it on one's computer, which was either standalone or part of an internal network. Nowadays, if one wants to look up restaurants on a search engine; find directions to a location; listen to music; watch a video; or sell product; all one needs is a computer with an Internet connection which can be manifest as a mobile telephone with access to a wireless network. Although these activities just require a digital device, none of the content one is accessing or the applications one is utilising may be actually stored on that local device -- instead they are stored at a giant data centre somewhere in the 'Computing Cloud'. And we don't give any of it a second thought! Just like we do not think twice about where the electricity is coming from when we plug an appliance into the wall. However, does the comparison between Digital Capital and electricity hold up to close scrutiny? No, not at all!

Brand Value & Code of Conduct

There is no question: the Personal Computer is giving way to a new era, the Utility Computing Age. However, it is naive to assume that Cloud Computing is like an electricity or gas utility. It is much more complex and risk prone because the outsourcing of sensitive Digital Capital is involved. Each electron or gas molecule is similar in utility to the next one, but this is not true for every byte of Digital Capital at all. Each Digital Capital byte may have unique characteristics. Digital Capital is the life blood of almost all organisations in the 21st century and is the crucial carrier of creativity, intellectual property, risk transfer as well as trust between parties. Contrary to popular myth, propagated in the context of cutting costs drastically, the reliability, availability, scalability and maintainability of Cloud Computing infrastructure and applications is still far from perfect. This leaves gaping holes, asymmetric threats and security risks in the areas of confidentiality, integrity, authentication and non-repudiation of outsourced Digital Capital storage, exchange and its transactions. Unless there is a code of conduct for handling Digital Capital by Cloud Computing vendors similar to bankers taking money deposits with independent regulatory oversight, we are setting ourselves up for huge national and corporate vulnerability in the 21st century. The strength of our organisations, manifest as brand value, is compromised by the weakest link. What if that weak link handles our Digital Capital and operates outside the control of our organisation and jurisdiction?

Asymmetric Security Hazards

Cloud Computing is fraught with asymmetric security hazards, which can cause havoc when manifest. A brand name built up over a century or more may lose credibility within a day. Why? Because the personal data of a million customer profiles with names, addresses, family member details, purchasing habits, has fallen into the wrong hands. Sound familiar? Digital Capital has unique and, in some cases, unquantifiable risk attributes. Hence, Cloud Computing requires risk assessment in critical areas such as data integrity, recovery, and privacy including identity management; and an evaluation of legal issues in areas such as electronic discovery, regulatory compliance and auditing.

Share Price Vulnerability

Recently, the Chief Information Officer, of a major transnational group decided not to rely entirely on business software from a long-established software vendor and IT integrator that would have let their group own the technology. Instead, the CIO rented these indispensable digital products from a Search Engine vendor via an unconventional approach called 'Cloud Computing'. The incentive to do so was clear: cut costs drastically given the global economic downturn. After lengthy internal testing, the CIO became convinced that the Search Engine vendor could be trusted to provide critical software programs. However, the CIO wrote an internal memo to the CEO -- at the request of the compliance department -- that should the data fall into the wrong hands, the inherent risk of Cloud Computing will boomerang swiftly on the share price of the listed company amongst other unintended consequences! When we label the CIO as Chief Information Officer, we have put him in charge of Information and associated technology in our mind, which we treat as similar to the handling of electricity, gas, telecom or other utilities. However, when we recognise that the CIO is actually handling the crown jewels of our enterprise, then we may be minded to call him CDC or Chief of Digital Capital!

Cloud Computing Tsunami

Cloud Computing is picking up significant traction, but before organisations jump on to the Cloud Computing bandwagon, they should consider the unique security risks this entails for their Digital Capital. The Cloud Computing wave is the most dramatic and critical challenge the mi2g* Intelligence Unit's (mIU) Bespoke Security Architecture (BSA) team and the ATCA* Research and Analysis Wing (A-RAW) have observed in the global business landscape since the original wave of the world wide web via the Internet in the mid-1990s. The original wave was about information dissemination, exchange and cyber transactions. However, Cloud Computing is going much further and significantly changing global business models by causing Digital Capital to be stored outside. In fact, the Cloud Computing wave is not just a wave, it has been compared to a Tsunami. What is causing this Cloud Computing Tsunami to unleash at such an accelerated pace despite the inherent asymmetric risks to an organisation's survival? Ask yourself this, what happens as in 2010 and beyond, organisations desperate to cut costs drastically:

. Forgo capital expenditures and instead purchase almost half of their IT infrastructure as an outsourced service; and

. Carry out at least half of the application software spending as a service subscription at a much reduced cost, instead of as a product license.

Unintended Consequences

Thanks to the thousands of miles of fibre-optic cable laid down during the late 1990s, the speed of computer networks has finally caught up with the speed of computer processors. What the fibre-optic Internet does for computing is exactly what the Alternating-Current (AC) network did for electricity. Suddenly, computers that were once incompatible and isolated are now linked in a grid-like giant network or 'Cloud'. As a result, computing is fast becoming a utility in much the same way that the electricity grid did at the start of the last century. Rendered obsolete, the traditional Personal Computer is replaced by a simple terminal -- a 'Thin Client' that is little more than a monitor hooked up to the Internet or a mobile telephone device accessing wireless networks. While that may sound far-fetched, in the corporate market, sales of 'Thin Clients' have been growing at over 20% per year -- far outpacing that of conventional PCs and sales of mobile devices have been growing exponentially. The simple truth is that Cloud Computing is becoming as big a part of our daily lives as much as mobile voice telephony and satellite navigation, albeit with unintended consequences for all forms of Digital Capital, identity management, corporate resilience, stakeholders' safety and security hazard.

Who are The Winners and Losers?

In 2010, and in the years ahead, many executive decision makers expect Cloud Computing to become much more attractive and loom ever larger on their board-of-directors' horizon. In contrast with software which requires installing programs on disparate computers, Cloud Computing lets organisations have someone else run their software remotely for a monthly or annual fee, with users accessing the programs over live Internet connections. Cloud Computing isn't just a modern convenience -- it is becoming an enormous industry. This technology is cutting billions in costs whilst showering billions in revenues on companies that purvey it. The question is: who are the winners and who are the losers? New players and the incumbents or other unknown actors? Everyone from individuals to government agencies and multinational corporations can now simply tap into the 'Cloud' to get all the things they used to have to supply and maintain themselves. As computing moves online, the sources of power and money are increasingly manifest as enormous Computing Clouds of Digital Capital! Who is going to secure them?

*mi2g, ATCA Open, The Philanthropia and HQR

Related Briefings

Digital Tribes: Rising Asymmetric Power

Resurrection: Are The Cloud, Collective Consciousness and The Singularity Intertwined?

The Rise of The Bio-Info-Nano Singularity

Systemic Crisis: The Rise of Machines, Casinos and Illiquidity

What Is the Key to Survival in a Constantly Changing Environment?

Are Black Swans Proliferating? You Decide!

Nanofood, Nanotech and Nanites: Quantum Effects and Fundamental Choices?

Butterfly Effect, Oil Gusher & Edge of Chaos: World Wide Summit?

Wireless Power: Has The Time Come?

The social media revolution has given way to a generation of tech-savvy and interconnected young Americans. Youthful social media users share their personal lives online, tweeting and posting everything from their relationship status to their current location to their latest purchases. Yet, when it comes to discussing deeper personal finance issues or seeking personal finance advice online, the majority of young adults typically shy away from the web.

AARP recently conducted a national study of young adults in the 18 to 34 age bracket; 57 percent of respondents said that money (specifically the burden of paying bills and carrying debt) was their primary concern. Facing a recession and a brutal job market, young adults are starting to pay more attention to their financial autonomy and planning, yet only 1 in 10 respondents reported sharing financial information or seeking financial advice through social media.

This is starting to change with the advent of trustworthy, unbiased online personal financial resources -- websites that enable users to monitor their own spending, create short-term and long-term financial plans and get trusted financial advice. In fact, 85 percent of young people who have used social media for personal finance advice have reported that doing so made them feel "more confident" about their finances.

These new financial resources are breaking down the taboo of sharing, discussing and managing personal finance online. Whether you are a tech-savvy, social media guru or someone who spends a limited amount of time on the web, you can very easily leverage the internet to gain a greater understanding of your personal finances in a few short steps.

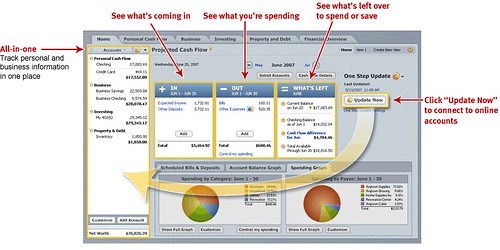

1. Make the most of online banking to make your life easier and keep your finances organized. Online banking is great because it offers quick, easy, 24-hour access to your checking and savings accounts. Here are three ways to make the most of online banking:

- Set up direct deposit for your paychecks so your salary (or other form of income) gets transferred directly and securely into your checking account.

- Set up online bill pay for your monthly bills -- your monthly payments will automatically be transferred from your checking account on a designated date each month. If you are not ready to commit to monthly bill pay or simply want to monitor your bills more closely, you can choose a one-time monthly payment. (*Remember to only set up automatic payments to companies or people you trust)

- Set up calendar alerts two to three days before your bills are due to remind you to pay on time -- never miss a payment or your credit history will take a hit.

2. Start utilizing trusted and unbiased personal finance sites to learn more about personal finances.

LearnVest and other personal financial sites help you manage and understand your finances through tools, games, discussion pages and often, targeted daily newsletters. Whether you need help figuring out how to open an IRA, pay down credit card debt and student loans or find the right health insurance for you and your family, these sites offer expert, step-by-step advice -- for free. Many of these sites employ financial experts to answer your questions or guide you through a financial issue.

3. Use these websites for financial advice pertaining to family life or career changes.

Whether you are preparing for a baby or changing jobs, these sites will help you understand and navigate your way through these life changes. Learn how to negotiate for a raise, handle a tricky situation with your colleague or boss, and choose the employee benefits that are right for you. While personal finance websites are small in number, most of them include live discussion pages (similar to Facebook or Twitter pages) where you can chat with other users whose financial circumstances are similar to your own. Ask users on the site about techniques they use to give themselves a financial advantage in the workplace or to maintain financial autonomy in their marriage.

4. Use social media to find great discounts and deals.

There are tons of discounts and deals to be found on the web. These range from Twitter-only deals from sites like AmazonMP3, JetBlueCheeps, CheapTweet to Promo Code Websites like RetailMeNot, Coupon Cabin, CouponChief.

The AARP study found that young people feel a pinch on their social budgets -- 69 percent say that they suggest low-budget entertainment options and 57 percent say that they sometimes skip going out with their friends for financial reasons. Use social networking to communicate with friends and share information to come up with fun, budget-friendly things to do.

5. Get online and get (free) help to get out of debt.

Many websites offer step-by-step guides to help you take the right steps to get out of debt. With these online checklists, you'll learn how to get a free credit report online (I recommend using creditkarma.com!) differentiate between good debt and bad debt, and take the necessary steps to pay down your credit card.

While I strongly encourage my readers to take advantage of the internet and social networking platforms to gain a greater understanding of their personal finances, it is extremely important to be safe, smart, and responsible when it comes to sharing, discussing, and managing your finances online. There are many random, unprotected sites online that appear safe to use and are ready to accept credit card information. You wouldn't give a stranger off the street your credit card information, so be extra cautious about who you are sharing it with online. For the most part, never share certain personal financial information, i.e. credit card information or bank account information, unless it is with your bank, or a site that you have confirmed is trusted, secure and password protected.

mike fuljenz mike fuljenz mike fuljenz mike fuljenz mike fuljenz mike fuljenzSome of you told us that you really liked it, especially how the "News for you" section lets you see a stream of articles tailored to the interests you specify. The positive usage data we saw during our months-long tests of the redesign ...

61 Responses to “News break”. 1. July 15th, 2010 at 5:12 pm. Joseph Nobles. Somebody's getting laid tonight. Reply. 2. July 15th, 2010 at 5:13 pm. beltane. There is already a diary up at GOS about how the Goldman Sachs settlement is ...

Tragic news coming off the wires, as footballing legend Emile Heskey – once described as the “most popular footballer of his generation” – has decided enough is enough, he can't take the adulation of playing for England any longer and ...

Note: the video is not showing on iPad.

Any chance of an alternative format (I assume the one on the page is in Flash)?

Thx.

Posted by readerOfTeaLeaves | July 9th, 2010 at 11:03 pm

Parents, Education, & Symptoms

Parents have got to get in the game, if they want to continue participating. The education system is an abject failure. It has to be replaced, and the tool is there to do it. Parents do not require permission from government or multinational corporations. Uncontrolled multinational growth is a function of community failure.

Of course the multinationals want nations, states, communities and individuals competing against each other; their controlling interests naturally breed on control. Of course they pay the economists to argue that competition is the be all and end all. On the one hand parents are competing in a system designed to ensure they lose, and on the other they attempt to give their own children a comparative advantage over other kids, locking failure in for the community.

The best thing parents can do is build strong, independent communities, so all kids can be successful. In net, parents are isolating their children into a competition with the multinationals, while their own governments are offering them a near-term profit to dissolve their families, paid for by the multinationals, which the governments are competing for, by giving them your money, your property, your taxes, and your ideas. And what makes it all work is parents competing to get in their cars and go shopping to feed the multinationals.

Economies are self-correcting. Multinationals cannot change their behavior. They destroy their own food chain, new families, by economic design. The multinationals are writing the laws, to which parents are subjected, and to which the multinationals are exempted, in a political system paid for by the parents. If the community is simply an extension of the State, the system may only liquidate. A constitution is designed to protect the State from itself. Only a community can protect liberty, and liberty is the path to the future.

Much of America is a victim of its own success. The multinationals have grown alongside strong communities. GDP measures consumption cost. It in no way measures investment or profit. The multinationals are simply a looking glass, and what parents see is what they want to see. Politicians tell parents whatever they want to hear, largely that the problem is government or corporate.

Yes. The more you shop, the longer it will take for the machine to target you, but the machine has caught up to everyone now. An American flag does not make a multinational American. Because some communities choose to be fat, dumb, and lazy in no way limits other communities. Liberty is not subject to majority vote. If a majority jumps off a bridge, will you?

Anything is fixable, if the right people are in charge. In this case, the parents have to take charge of the economy. There is always a reservoir of goodwill for children somewhere. When you have ruled everything else out, what remains, no matter how improbable, is the solution. Not so ironically, Barack Obama was a community organizer.

So long as those cleats hold onto the bank, and you have a good strong rope of small businesses, we’ll pick that $500T load.

Right now, your problem is RICO organization of multinationals through every level of government to preempt participation by small family businesses, to backfill the economy.

Posted by kevinearick | July 10th, 2010 at 4:26 pm

@readerOfTeaLeaves Unfortunately the video we embedded is from GRIT’s site, and they put it up in flash, so there’s not much we can do. Sorry I can’t be of more help!

Posted by Bryce | July 12th, 2010 at 10:57 am

Thanks Bryce. I came back and viewed it on a ‘not-an-iPad’, but appreciate your explanation.

Posted by readerOfTeaLeaves | July 12th, 2010 at 5:41 pm